Insuring properties in hazard-prone markets, such as homes located near wildfire risk areas, requires a specialized approach to risk analysis. The stakes are high, and the potential for catastrophic losses makes it crucial for insurers to leverage advanced analytics. In this blog post, we’ll explore the top analytics tools and techniques that are essential for effectively assessing and managing risks in these high-risk environments.

1. Geospatial Risk Analysis

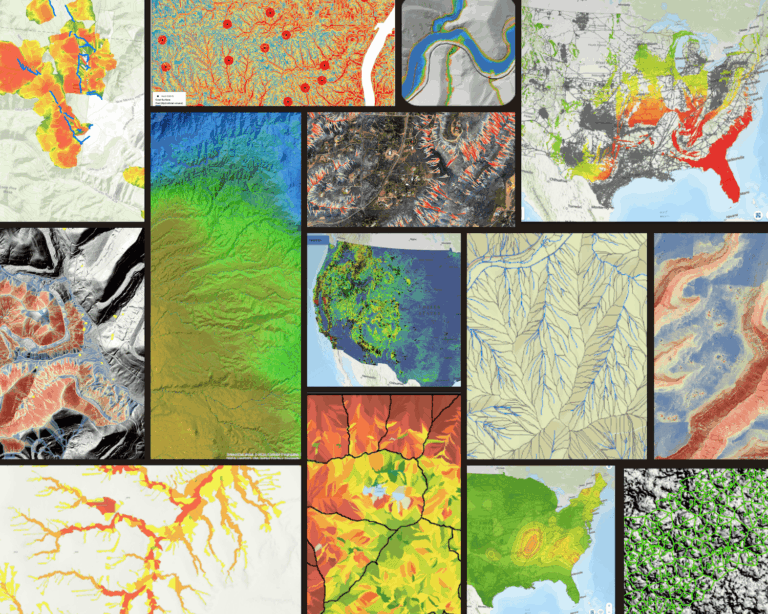

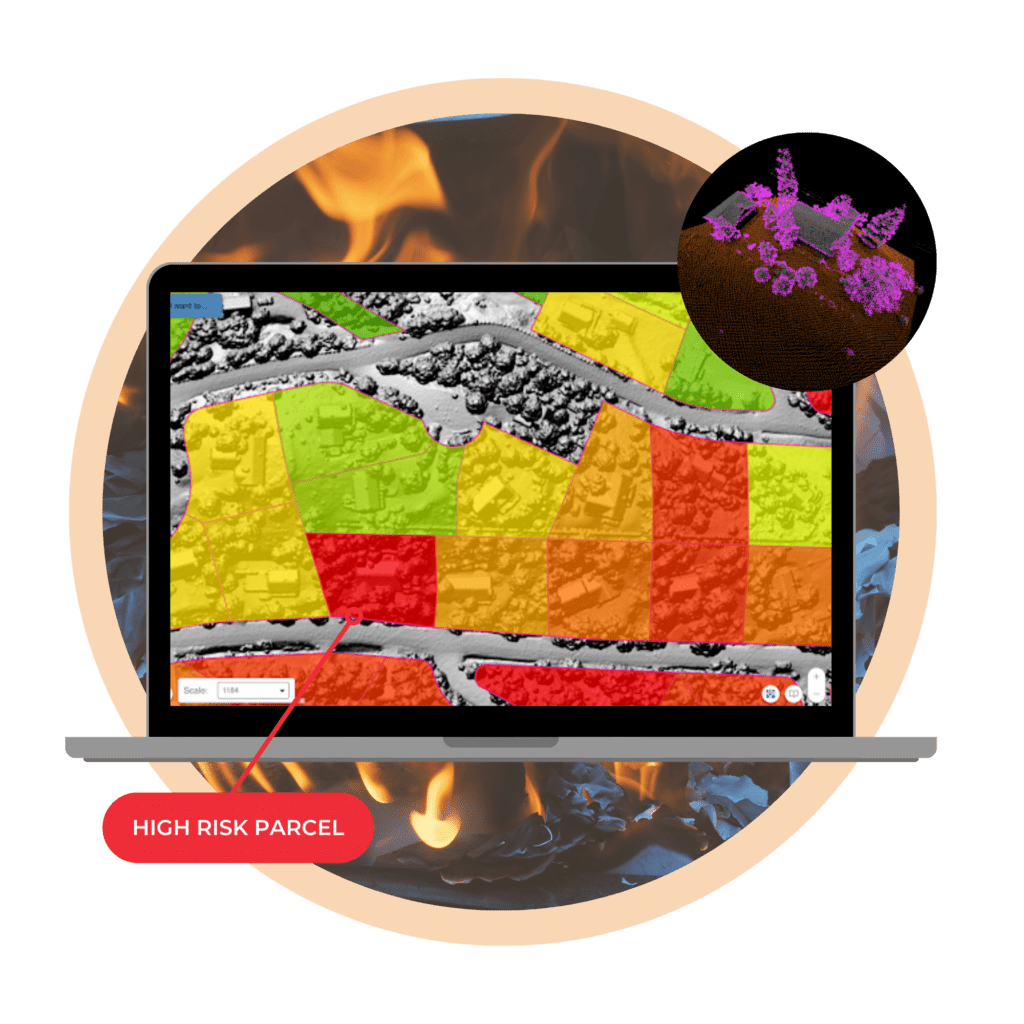

When it comes to properties near wildfire-prone areas, geospatial risk analysis is indispensable. Wildfire risk mapping is a key tool that uses advanced geospatial analytics to assess the proximity of insured properties to high-risk zones. By analyzing historical wildfire data, vegetation types, topography, and climate patterns, insurers can predict future fire risks with greater accuracy.

In addition to wildfire risk, environmental hazard modeling provides a comprehensive risk profile by assessing the potential impact of other natural hazards such as floods, earthquakes, and landslides. This holistic approach ensures that insurers have a full understanding of the environmental risks each property faces.

2. Catastrophe Modeling

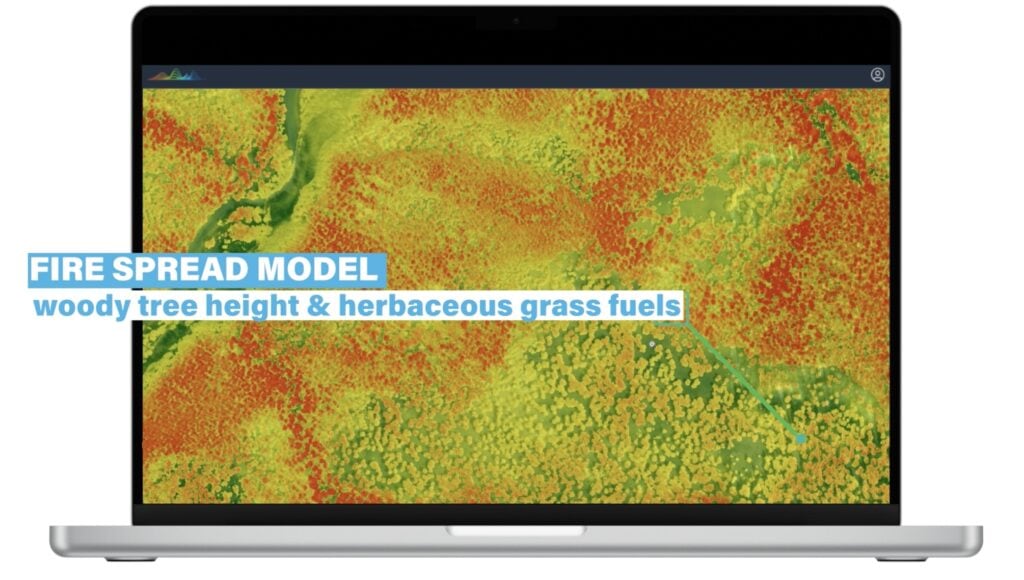

Catastrophe modeling is essential for estimating potential losses from large-scale disaster events. Fire spread simulation is a powerful tool that helps insurers understand how wildfires might propagate through different landscapes. By considering factors like wind patterns, fuel load, and weather conditions, these models can predict the extent and severity of potential wildfire damage.

Additionally, scenario analysis allows insurers to run “what-if” scenarios that evaluate the financial impact of various disaster scenarios. For example, they can assess the potential losses from a worst-case wildfire event during peak dry seasons. This information helps insurers prepare for the financial implications of extreme events.

3. Remote Sensing and Monitoring

The use of remote sensing technology is revolutionizing risk assessment in hazard-prone areas. Satellite, LiDAR and drones provide real-time monitoring of fire conditions, vegetation health, and changes in land use around insured properties. This data enables insurers to perform dynamic risk assessments and offer early warnings of potential threats.

Moreover, sensor data integration enhances the accuracy of fire risk assessments. By incorporating data from ground-based sensors, such as weather stations and air quality monitors, insurers can gain a deeper understanding of fire behavior and environmental conditions.

4. Predictive Analytics for Loss Prevention

Preventing losses is just as important as predicting them. Predictive risk scoring models help insurers forecast the likelihood of a property being affected by a wildfire. These models use a combination of historical data, current environmental conditions, and property characteristics to assess risk levels.

In addition to predicting risks, insurers can provide loss mitigation recommendations to property owners. These insights may include actions such as creating defensible space, using fire-resistant materials, and maintaining proper vegetation management. By taking these proactive steps, property owners can reduce their risk, and insurers can lower the likelihood of costly claims.

5. Claims Data Analytics

After a wildfire event, analyzing claims data is essential for refining future risk assessments. Post-event loss analysis helps insurers understand loss patterns and improve underwriting criteria. By studying the outcomes of previous events, insurers can better prepare for future risks.

In high-risk areas, fraud detection becomes particularly important. Using machine learning and data analytics, insurers can identify fraudulent claims that may arise in the aftermath of a disaster. This ensures that resources are allocated to genuine claims, protecting the insurer’s financial stability.

6. Regulatory Compliance and Reporting

Regulatory compliance is a critical aspect of insuring properties in hazard-prone markets. Regulatory risk analysis ensures that underwriting practices and risk models meet state and federal requirements, especially in high-risk areas where special rules may apply.

Moreover, disaster preparedness reporting provides detailed information to regulatory bodies and stakeholders about the insurer’s exposure to wildfire risks and the measures being taken to mitigate those risks. This transparency helps build trust and ensures that the insurer remains compliant with all relevant regulations.

Conclusion

Insuring properties in hazard-prone markets, such as homes near wildfire risk areas, requires a specialized set of analytics tools that go beyond traditional risk assessment methods. From geospatial to claims data analysis, these analytics are essential for accurately assessing risks, pricing policies, and managing exposure in markets where the stakes are high.

Webinar: Settling the Score on Wildfire Risk

To learn more on this topic, check out Teren’s recent webinar with EigenRisk: Settling the Score on Wildfire Risk.